Factory Building Depreciation Rate . [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that: a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. Read about land and building. While calculating depreciation for building under income tax, the following above blocks can be formed for the. (i) the lining element (allocated cost $50,000 with a useful life of five years), and. for residential premises, depreciation of up to 5% per year is allowed for taxation. the asset has two depreciable components: this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. depreciation rate for building.

from www.chegg.com

[ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that: the asset has two depreciable components: While calculating depreciation for building under income tax, the following above blocks can be formed for the. Read about land and building. a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. for residential premises, depreciation of up to 5% per year is allowed for taxation. depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. depreciation rate for building. (i) the lining element (allocated cost $50,000 with a useful life of five years), and.

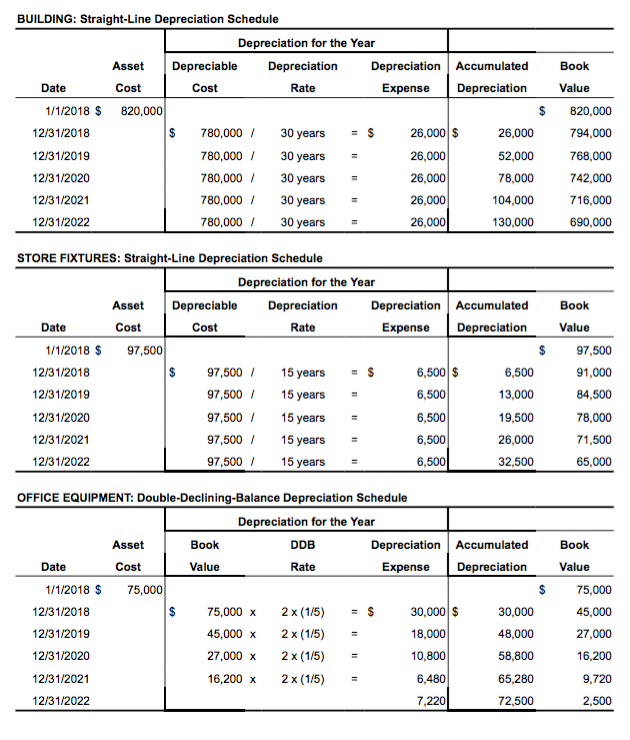

Solved BUILDING StraightLine Depreciation Schedule

Factory Building Depreciation Rate depreciation rate for building. While calculating depreciation for building under income tax, the following above blocks can be formed for the. a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. (i) the lining element (allocated cost $50,000 with a useful life of five years), and. Read about land and building. the asset has two depreciable components: depreciation rate for building. depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. for residential premises, depreciation of up to 5% per year is allowed for taxation. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that: this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite.

From studylib.net

Depreciation Rates Factory Building Depreciation Rate this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. depreciation rate for building. Read about land and building. for residential premises, depreciation of up to 5% per year is allowed for. Factory Building Depreciation Rate.

From mungfali.com

Depreciation Rate Factory Building Depreciation Rate depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. Read about land and building. a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. this chapter discusses various aspects of accounting for depreciation of tangible assets. Factory Building Depreciation Rate.

From www.fastcapital360.com

How to Calculate MACRS Depreciation, When & Why Factory Building Depreciation Rate the asset has two depreciable components: While calculating depreciation for building under income tax, the following above blocks can be formed for the. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that: a variety of depreciation methods can be used to allocate the depreciable amount of an asset. Factory Building Depreciation Rate.

From www.educba.com

Depreciation for Building Definition, Formula, and Excel Examples Factory Building Depreciation Rate a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. (i) the lining element (allocated cost $50,000 with a useful life of five years), and. depreciation rate. Factory Building Depreciation Rate.

From www.chegg.com

Solved 8. The depreciation rate on factory equipment is Factory Building Depreciation Rate (i) the lining element (allocated cost $50,000 with a useful life of five years), and. While calculating depreciation for building under income tax, the following above blocks can be formed for the. the asset has two depreciable components: Read about land and building. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it. Factory Building Depreciation Rate.

From www.wallstreetprep.com

What is Depreciation? Expense Formula + Calculator Factory Building Depreciation Rate (i) the lining element (allocated cost $50,000 with a useful life of five years), and. this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. [ias 16.3] items of property, plant, and equipment. Factory Building Depreciation Rate.

From www.bmtqs.com.au

Fixtures & Fittings Depreciation Rate BMT Insider Factory Building Depreciation Rate (i) the lining element (allocated cost $50,000 with a useful life of five years), and. for residential premises, depreciation of up to 5% per year is allowed for taxation. Read about land and building. While calculating depreciation for building under income tax, the following above blocks can be formed for the. this chapter discusses various aspects of accounting. Factory Building Depreciation Rate.

From haipernews.com

How To Calculate Depreciation As Per Companies Act Haiper Factory Building Depreciation Rate depreciation rate for building. this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. Read about land and building. for residential premises, depreciation of up to 5% per year is allowed for taxation. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable. Factory Building Depreciation Rate.

From iteachaccounting.com

Depreciation Tables Factory Building Depreciation Rate for residential premises, depreciation of up to 5% per year is allowed for taxation. this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. the asset has two depreciable components: depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. [ias. Factory Building Depreciation Rate.

From www.bmtqs.com.au

What Is A Depreciation Rate BMT Insider Factory Building Depreciation Rate for residential premises, depreciation of up to 5% per year is allowed for taxation. (i) the lining element (allocated cost $50,000 with a useful life of five years), and. a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. [ias 16.3] items of property, plant,. Factory Building Depreciation Rate.

From thirdspacelearning.com

Depreciation GCSE Maths Steps, Examples & Worksheet Factory Building Depreciation Rate a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. (i) the lining element (allocated cost $50,000 with a useful life of five years), and. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that: Read about land. Factory Building Depreciation Rate.

From corporatefinanceinstitute.com

Depreciation Schedule Guide, Example of How to Create a Schedule Factory Building Depreciation Rate a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that: for residential premises, depreciation of up to 5% per year is allowed for taxation. the asset. Factory Building Depreciation Rate.

From cryptolisting.org

5 Steps to Calculate Units of Production Depreciation Coinranking Factory Building Depreciation Rate depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. a variety of depreciation methods can be used to allocate the depreciable amount of an asset on a systematic basis over its. While calculating depreciation for building under income tax, the following above blocks can be formed for the. (i). Factory Building Depreciation Rate.

From www.exceldemy.com

How to Use WDV Method of Depreciation Formula in Excel Factory Building Depreciation Rate depreciation rate for building. this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. Read about land and building. the asset has two depreciable components: [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that: (i) the lining element (allocated cost $50,000. Factory Building Depreciation Rate.

From www.legalraasta.com

Depreciation Rate For Plant, Furniture, and Machinery Factory Building Depreciation Rate depreciation rate for building. for residential premises, depreciation of up to 5% per year is allowed for taxation. this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. the asset has two depreciable components: Read about land and building. a variety of depreciation methods can be used to allocate. Factory Building Depreciation Rate.

From corporatefinanceinstitute.com

Straight Line Depreciation Formula, Definition and Examples Factory Building Depreciation Rate this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of finite. the asset has two depreciable components: While calculating depreciation for building under income tax, the following above blocks can be formed for the. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable that:. Factory Building Depreciation Rate.

From www.online-accounting.net

Straight Line Depreciation Method Online Accounting Factory Building Depreciation Rate for residential premises, depreciation of up to 5% per year is allowed for taxation. depreciation rate for building. depreciation is a mandatory deduction in the profit and loss statements of an entity using depreciable assets and. Read about land and building. this chapter discusses various aspects of accounting for depreciation of tangible assets and amortization of. Factory Building Depreciation Rate.

From owlcation.com

Methods of Depreciation Formulas, Problems, and Solutions Owlcation Factory Building Depreciation Rate Read about land and building. While calculating depreciation for building under income tax, the following above blocks can be formed for the. depreciation rate for building. for residential premises, depreciation of up to 5% per year is allowed for taxation. [ias 16.3] items of property, plant, and equipment should be recognised as assets when it is probable. Factory Building Depreciation Rate.